The average retiree in 2026 has saved $288,700. Ask that same person how much they think they need, and most say $823,800. That gap is the reason this calculator exists, and it is worth running before you make any other retirement decision.

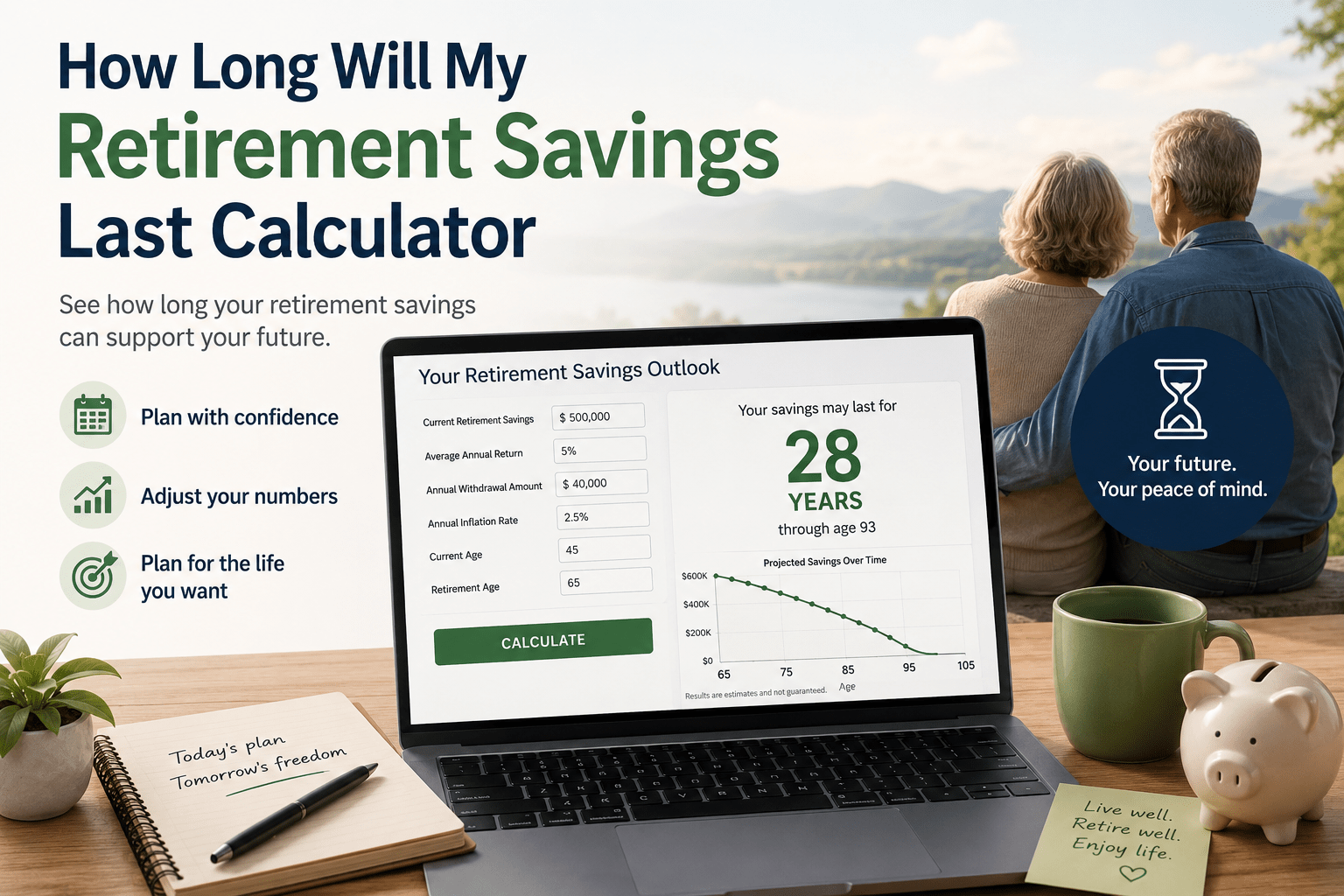

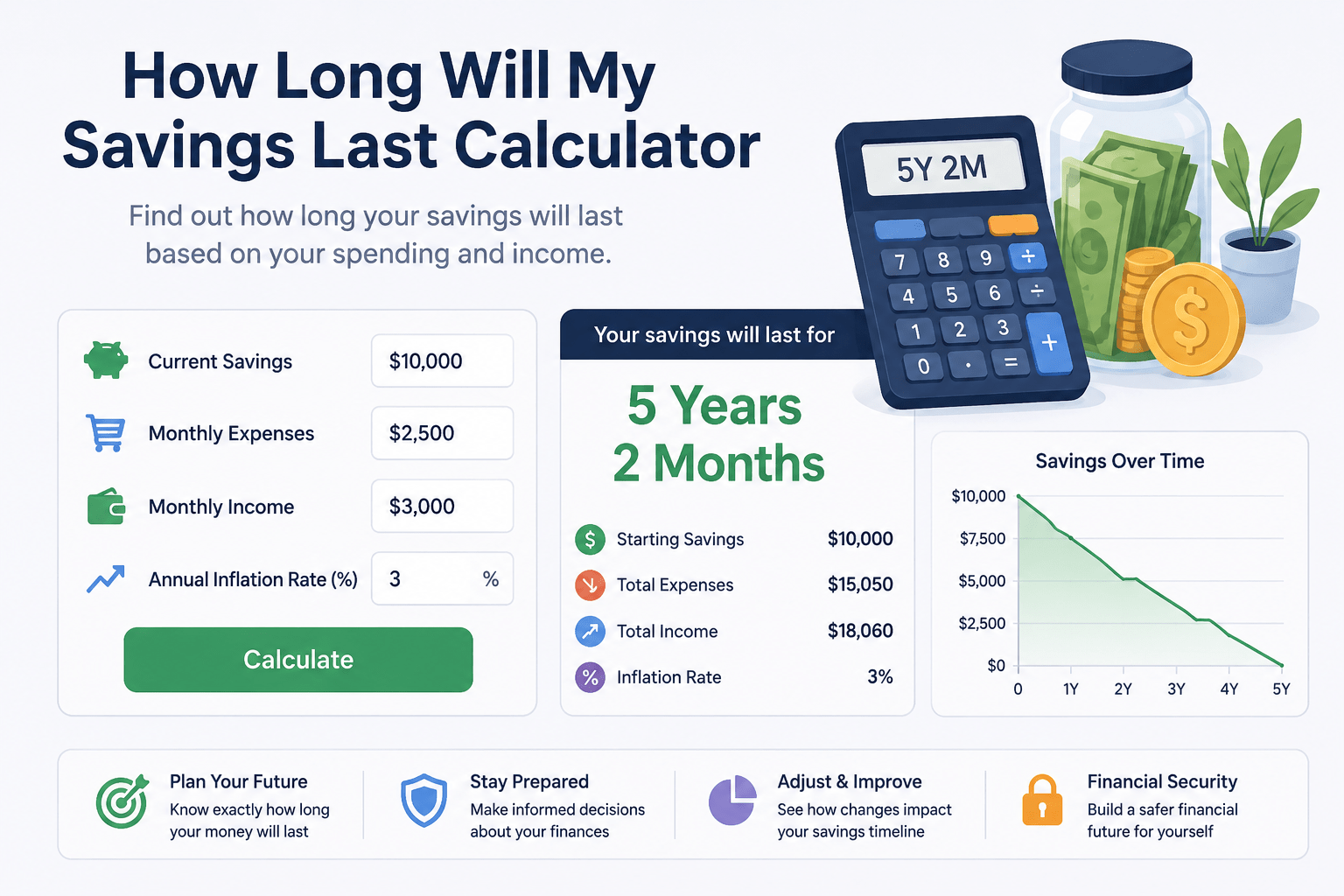

How Long Will My Savings Last?

Enter your numbers to see your retirement runway

- Delay Social Security to 70. Each year past full retirement age adds 8% to your monthly benefit permanently.

- Keep withdrawal rate at or below 4%. The difference between 4% and 6% can cost 10 to 15 years of runway.

- Maintain equity exposure. A portfolio with no stocks often cannot outpace inflation over 25 to 30 years.

- Reduce spending in down-market years. Even a 10% cut in bad years preserves compounding capital for the recovery.

- Consider relocating. $1 million lasts 12 years in Hawaii but over 80 years in Mississippi based on cost-of-living data.

This calculator provides estimates only. It does not account for taxes, required minimum distributions, healthcare cost spikes, or variable market conditions. Consult a licensed financial advisor before making retirement decisions.

This guide walks through how the calculator works, which numbers actually move the result, and what you can do if the answer is shorter than you hoped.

What’s in this guide

- What the calculator actually does

- The numbers you need before you start

- The 4% rule, and where it breaks down

- How long different savings amounts actually last

- What shortens or extends your runway

- How to make your savings last longer

- Where Social Security fits in

- Common questions

What the calculator actually does

A savings duration calculator takes your balance, your withdrawal rate, your expected return, and an inflation assumption, and tells you when the account hits zero. That is the whole function.

The math behind it is simple. Each month, your balance earns a slice of your annual return. Then your withdrawal comes out. The calculator repeats this until the balance hits zero, counts the months, and converts that into years.

The variable that moves the result most is your monthly withdrawal. Cut $200 a month from a $500,000 portfolio earning 5%, and you add roughly 3 to 4 years before the money runs out. That is worth knowing before you retire, not after.

To run the calculation yourself, you need five numbers:

- Your total retirement savings balance (all accounts combined)

- Your expected monthly withdrawal amount

- Other monthly income (Social Security, pension, rental income)

- Your expected annual investment return

- An inflation rate assumption (3% to 4% is reasonable for 2026 planning)

The numbers you need before you start

Before you open a calculator, get your numbers right. A wrong input here either scares you unnecessarily or gives you false confidence.

Total savings balance. Add up every retirement account: 401(k), IRA, Roth IRA, taxable brokerage accounts, and any savings set aside for retirement. Leave out home equity unless you plan to sell.

Monthly withdrawal amount. Start with your current monthly expenses, then adjust. Some costs drop in retirement, like commuting. Others climb, like healthcare and travel. The Bureau of Labor Statistics put average household spending at $77,280 in 2023, or about $6,440 a month. Your own number could be higher or lower depending on where you live and how you spend.

Monthly income from other sources. Subtract your expected Social Security benefit, pension, rental income, or annuity payments from your monthly spending need. What is left is the amount your savings actually have to cover. The average Social Security benefit for retired workers in 2026 runs about $2,071 a month. If your expenses are $4,500 and Social Security pays $2,071, your savings only need to cover $2,429.

Investment return. A balanced portfolio of stocks and bonds has historically returned 5% to 6% a year. A heavier equity allocation might project 7%. Use the lower end once you are already retired, since there is less time left to recover from a bad stretch in the market.

Inflation rate. US inflation was running around 3.8% in April 2026. For long-term planning, 3% is a common default, though some planners use 3.5% as a cushion.

The 4% rule, and where it breaks down

The 4% rule is the shortcut most people reach for first. Financial advisor William Bengen developed it in 1994. He found that a portfolio with 50% to 75% in stocks, the rest in bonds, could support annual withdrawals of 4% of the starting balance, adjusted upward for inflation each year, for at least 30 years.

In practice: with $1 million saved, you withdraw $40,000 in year one. If inflation runs 3% the next year, you withdraw $41,200 in year two. You keep raising that number regardless of what the market does.

Morningstar revisited the rule in its 2025 State of Retirement Income report and set the safe rate at 3.9% for today’s retirees. Kiplinger reported in June 2026 that inflation was running at 3.8% annually, which puts real pressure on a fixed withdrawal plan in the early years of retirement.

The rule has real limits:

- It assumes a 30-year retirement. Retire at 55, or live past 90, and the math no longer fits.

- It does not flex for heavy spending early on or lighter spending later.

- It ignores taxes. Withdrawals from a traditional 401(k) or IRA get taxed as ordinary income.

- It says nothing about sequence of returns risk, where a bad market in the first two or three years can do damage the portfolio never fully recovers from.

Treat the 4% rule as a starting point, not a verdict. Run your own numbers through a calculator to see how they hold up.

How long different savings amounts actually last

These scenarios use a 4% withdrawal rate, a 5% to 6% annual return, and 3% annual inflation adjustments. Social Security is left out on purpose, so you can see what the savings alone are doing. Your real numbers will move around depending on the market, so use these as a sense of scale, not a forecast.

$300,000 in savings

At a 4% withdrawal rate, that is $12,000 a year, or $1,000 a month, coming out of savings. At a 5% return, the balance lasts roughly 34 to 38 years. But most retirees need more than $1,000 a month to live on. Push withdrawals to $3,000 a month (a 12% rate), and $300,000 is gone in 9 to 10 years. This is exactly why Social Security matters so much for people with smaller balances.

$500,000 in savings

With $500,000 and withdrawals of $20,000 a year, the 4% rate, savings last roughly 25 to 30 years at a 5% return. Push that to $30,000 a year, and the money runs out closer to age 85 for someone who retires at 70. Add Social Security to the mix and this picture changes substantially.

$1 million in savings

A 6% return with $5,000 a month in after-tax withdrawals (24% tax bracket) makes $1 million last roughly 24 years. Drop the return to 5% under the same withdrawal, and it lasts about 20 years. At a 4% withdrawal rate with a 7% return, $1 million can stretch past 36 years.

Location matters as much as the math. A GOBankingRates analysis found that $1 million combined with Social Security lasts just 12 years in Hawaii but over 80 years in Mississippi once cost of living is factored in. Where you retire may be the single biggest financial decision you make.

$1.5 million in savings

A $1.5 million portfolio has more room to breathe. At a 4% withdrawal rate, that’s $60,000 a year, and at a 5% return, the balance should last 30 years or more. At this size, running out of money is not really the risk. Inflation and unexpected healthcare costs eating into purchasing power later in retirement are.

What shortens or extends your runway

Your withdrawal rate

This is the one lever you fully control. Going from a 4% to a 6% withdrawal rate isn’t just 50% more spending; it often costs you 10 to 15 years of runway. Every extra dollar you pull out keeps compounding against you.

Sequence of returns risk

Retire right before a market downturn and the losses in years one through three eat a bigger share of your portfolio than the same losses would later, after you’ve had years to compound gains. Take two retirees who each start with $1 million and plan to withdraw $45,000 a year, adjusted 3% for inflation. The one who retires into a falling market can run out 5 to 10 years sooner than the one who retires into a rising one, even if both see the same average return over 20 years.

Inflation

A 2% inflation rate sounds harmless, but it shrinks $1 million in cash to about $603,465 of real purchasing power over 25 years. At 3%, the erosion is worse. Keep your withdrawals flat and you lose real income every year. Raise them with inflation and your savings drain faster in dollar terms. There’s no way around the tradeoff, only a choice about which side of it you’d rather manage.

Healthcare costs

Roughly 70% of Americans 65 and older will need some form of long-term care. A semi-private nursing home room runs about $111,325 a year. None of that shows up in a basic withdrawal calculator. Budget for it separately, or look at long-term care insurance.

Longevity

The Social Security Administration puts average life expectancy for a 65-year-old at 84 for men and 87 for women, and one in four 65-year-olds lives past 90. Plan for a 20-year retirement and live 30, and you’re short by a decade. A 65-year-old man should plan to at least age 90, and a 65-year-old woman to at least 92, since roughly a quarter of each group lives that long.

How to make your savings last longer

Keep your withdrawal rate at or below 4%

This is the most direct control you have. If your portfolio can’t support a 4% withdrawal without draining faster than planned, you have three options: spend less, find more income, or work longer. Morningstar’s 2025 analysis found that even conservative retirees holding 30% in equities could safely start at a 3.8% to 3.9% withdrawal rate.

Use a bucket strategy

Split your savings into three buckets. Bucket one covers 1 to 2 years of expenses in cash or money market funds. Bucket two covers 3 to 7 years in bonds and stable assets. Bucket three holds your long-term growth investments in equities. When the market drops, you spend from buckets one and two instead of selling stocks at a loss, which keeps your long-term bucket insulated from sequence of returns risk.

Cut spending in down market years

Trim discretionary spending by 10% to 15% in a year your portfolio drops 15% to 20%, and you preserve capital that compounds back during the recovery. Keep 1 to 2 years of expenses in cash so you’re never forced to sell stocks at a loss just to pay bills.

Delay Social Security to 70

Every year you delay past your full retirement age (67 for anyone born in 1960 or later) adds 8% to your benefit. A high earner who retires at 62 but waits until 70 to claim gets roughly $2,277 more a month than if they’d claimed at 62, per the Social Security Administration. That extra guaranteed income takes real pressure off your portfolio.

Keep some equity exposure

Many retirees move too heavily into bonds and cash, which caps long-term returns and leaves them exposed to inflation over a 25 to 30 year retirement. A portfolio with no stocks at all struggles to keep pace with inflation or rising healthcare costs over that long a stretch. A financial advisor can help you land on an allocation that fits your risk tolerance.

Consider relocating

Where you live in retirement is one of the bigger financial choices you’ll make. Moving from California to a state in the Midwest or South can cut your cost of living by 20% to 40%. That alone can add a decade or more to how long your savings last.

Where Social Security fits in

For most retirees, Social Security isn’t extra, it’s the floor everything else sits on. The average retired worker gets about $2,071 a month in 2026, according to the Social Security Administration. That’s roughly $24,852 a year, guaranteed and adjusted for inflation.

Here’s what that means in practice. A retiree with $500,000 in savings who needs $4,000 a month only has to pull $1,929 from savings after Social Security kicks in. That’s a withdrawal rate of about 4.6%, borderline but workable. Skip Social Security and pull the full $4,000 from savings, and the rate jumps to 9.6%. At that pace, $500,000 is gone in 10 to 12 years.

For married couples, the math works even harder in your favor. The Social Security Administration notes that it’s common for one spouse in a married couple to live into their 90s. Two benefit checks, especially if the higher earner waited until 70 to claim, can cover a large share of monthly expenses and leave savings largely untouched.

Even so, 64% of Americans say they’re more afraid of outliving their savings than of dying, according to the 2025 Allianz Annual Retirement Study. That fear isn’t unfounded, but it often comes from leaving Social Security out of the picture entirely.

About 51% of current retirees say they have no plan for what happens if their savings run out, per 2026 research from Clever Real Estate. That’s a planning gap more than a savings gap. Run the calculator, then layer your Social Security estimate on top of it, and the picture usually looks less grim than the headline numbers suggest.

Common questions

How do I calculate how long my savings will last?

You need four numbers: your balance, your monthly withdrawal, your expected return, and an inflation rate. Plug those into a calculator and it tells you how many years pass before the balance hits zero. As a gut check, the 4% rule says savings withdrawn at that rate should last about 30 years.

How long will $500,000 last in retirement?

Around 20 to 25 years if you’re withdrawing 4% a year and earning a reasonable return. Bring Social Security into the equation and you’ll likely stretch well past that, since less money needs to come out of savings each month.

How long will $1 million last in retirement?

Somewhere between 20 and 24 years if you’re withdrawing $5,000 a month after tax, depending on whether your return is closer to 5% or 6%. But the bigger swing factor might be your zip code: the same $1 million stretches 12 years in Hawaii and over 80 in Mississippi.

What is the 4% rule for retirement withdrawals?

It’s a 1994 rule of thumb from advisor William Bengen: withdraw 4% of your portfolio the first year, then bump that dollar figure up with inflation every year after. It was built to survive a 30-year retirement. Morningstar now puts the safer number closer to 3.9%.

What factors affect how long my savings will last?

Mostly your withdrawal rate and your return, but inflation, where you retire, healthcare costs, and when the market happens to dip all play a part too. Two retirees with identical savings can end up years apart in outcome just based on market timing.

How can I make my retirement savings last longer?

Spend less from savings, delay Social Security if you can afford to, don’t abandon stocks entirely, and have a cash buffer so you’re not selling investments at a loss during a downturn.