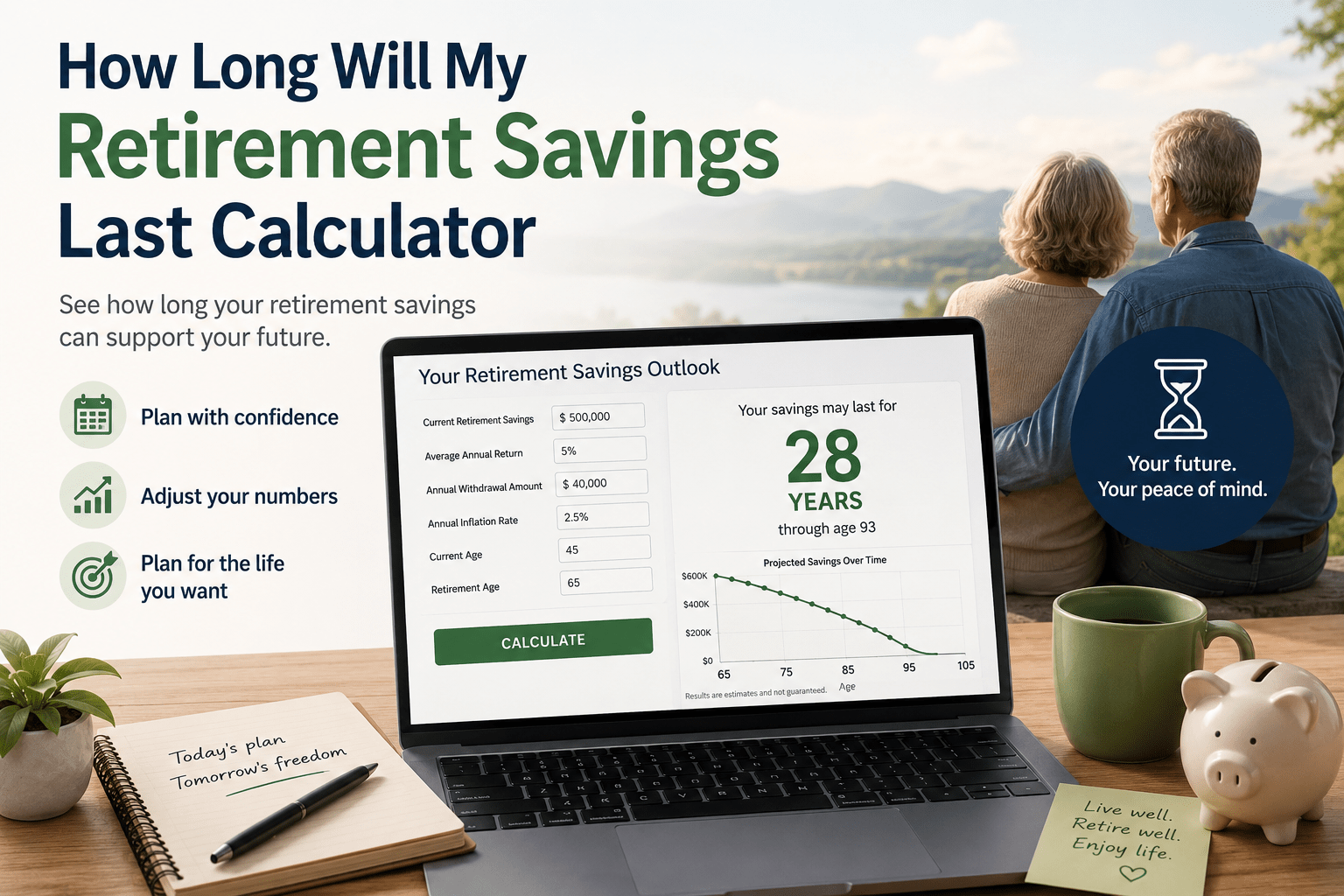

Using a how long will my retirement savings last calculator is one of the most important financial moves you can make before or during retirement. It gives you a concrete number: how many years your money will cover your lifestyle, based on real inputs like your balance, spending, and investment returns.

Without this calculation, you are guessing. And guessing wrong in either direction costs you. Retire too conservatively and you under-live your savings. Withdraw too aggressively and you run out of money at 79.

This guide walks you through how these calculators work, what inputs matter most, and what the results should tell you about your retirement plan.

How Long Will My Retirement Savings Last Calculator

Table of Contents

- Why You Need a Retirement Savings Duration Calculator

- The Inputs Every Calculator Needs

- Step-by-Step: How to Use the Calculator

- The 4% Rule and the 2026 Update

- Real-World Examples

- Factors That Drain Savings Faster Than Expected

- How to Make Your Savings Last Longer

- Frequently Asked Questions

- Conclusion

Why You Need a Retirement Savings Duration Calculator

A 65-year-old man in the U.S. can expect to live to around 83. A 65-year-old woman can expect to live to 85 or older. If you retire at 62, the current average retirement age, your savings need to stretch 20 to 25 years, possibly more.

The numbers confirm this is a real problem. The median American aged 55 to 64 has $185,000 in retirement savings. At even a modest $3,000 per month in withdrawals, that balance lasts about five years. Social Security helps, but the average monthly retirement benefit was $1,877 as of late 2024. For most people, that gap is significant.

A retirement savings duration calculator closes the guesswork. It takes your specific balance, spending, and income, and tells you exactly when the money runs out, or better, confirms that it will not.

The Inputs Every Calculator Needs

Most retirement savings calculators use five core inputs. Understanding each one helps you enter accurate numbers and interpret results correctly.

1. Current savings balance. This is the total across all retirement accounts: 401(k), IRA, Roth IRA, brokerage accounts, and any other savings you plan to draw from. Use the current balance, not a projected future value.

2. Monthly spending in retirement. Estimate what you will spend per month in retirement. A common starting point is 70% to 80% of your pre-retirement income, but this varies widely. Someone with a paid-off home and low travel plans spends differently than someone with a mortgage and an active lifestyle.

3. Other income sources. Include Social Security, pension payments, part-time income, or rental income. These reduce how much you need to withdraw from your portfolio each month, which directly extends how long your savings last. Enter your Social Security estimate from ssa.gov for the most accurate figure.

4. Expected rate of return. This is the annual growth rate you expect your portfolio to earn. A balanced portfolio of 60% stocks and 40% bonds has historically returned around 6% to 7% annually over long periods. Do not use the S&P 500's recent 10-year figure of 12.5% as your baseline. Use a conservative 5% to 7% for planning.

5. Inflation rate. Inflation reduces the purchasing power of every dollar you withdraw. A rate of 2.5% to 3% is a standard assumption. Healthcare inflation runs higher, closer to 5.8% per year, so if you have significant medical expenses, use a higher number.

Step-by-Step: How to Use the Calculator

Follow these steps to get a useful result from any retirement savings duration calculator.

Step 1: Gather your account balances. Log into each account and note the current balance. Add them together for a single total.

Step 2: Estimate your monthly retirement budget. List your expected monthly expenses: housing, food, transportation, healthcare, travel, and discretionary spending. Be honest. Many retirees underestimate expenses in early retirement when they are active and traveling.

Step 3: Add your guaranteed income. Check your Social Security statement for an estimate at your planned retirement age. Add any pension or rental income. Subtract this total from your monthly budget. The remainder is what your savings must cover each month.

Step 4: Set your return and inflation assumptions. Use 5% to 6% for investment returns and 3% for general inflation unless your spending is heavily weighted toward healthcare, in which case use 4% to 5%.

Step 5: Run the calculation and test scenarios. Enter your numbers and note the result. Then test these scenarios: What happens if you spend 10% more per month? What if your return drops to 4%? What if you delay Social Security by two years? Testing scenarios reveals how sensitive your plan is to each variable.

Step 6: Adjust your plan based on results. If the calculator shows your savings run out at 79 and you expect to live to 88, you have a gap to close. Your options are to save more, spend less in retirement, delay retirement, delay Social Security, or adjust your investment allocation.

The 4% Rule and the 2026 Update

For decades, the 4% rule served as the standard benchmark for retirement withdrawals. Financial planner William Bengen introduced it in 1994 after analyzing historical market data. The rule states that withdrawing 4% of your portfolio in year one, then adjusting for inflation each year, gives a strong probability of your money lasting 30 years.

In 2026, the guidance has been updated. Morningstar's State of Retirement Income report recommends a 3.9% starting withdrawal rate for retirees seeking inflation-adjusted income with a 90% probability of success over a 30-year retirement. This applies to portfolios holding 30% to 50% in equities.

In practical terms: if you have $1,000,000 saved, the research supports withdrawing $39,000 in year one, roughly $3,250 per month. If your spending plan requires $5,000 per month, your savings alone will not cover it at this rate. You either need more saved, lower spending, or more guaranteed income from Social Security or a pension.

Retirees willing to use flexible withdrawal strategies, meaning they reduce spending when markets drop and increase it when markets rise, can safely start at up to 5.7%, according to the same Morningstar research.

Real-World Examples

These examples show how the calculator works across different situations.

Example 1: The comfortable retiree. Maria, 65, retires with $800,000 saved. She expects $2,200 per month from Social Security and plans to spend $4,500 per month total. That means she needs $2,300 per month from her portfolio. Annualized, she withdraws about $27,600 per year, a 3.45% withdrawal rate. With a 6% return assumption and 3% inflation, her savings last well past age 95.

Example 2: The gap scenario. James, 62, retires with $300,000 saved. He receives $1,600 per month from Social Security and plans to spend $4,200 per month. He needs $2,600 per month from his portfolio, or $31,200 per year, a 10.4% withdrawal rate. At that rate, his savings run out in under 12 years, at age 74. The calculator flags a serious gap, and James needs to either reduce spending, delay retirement, or find additional income.

Example 3: The healthcare variable. Sandra, 67, has $650,000 saved and a $1,900 Social Security benefit. She spends $3,800 per month but has a chronic condition that drives healthcare costs of $800 per month above average. Using a 5.5% healthcare inflation assumption alongside standard 3% general inflation, the calculator shows her savings depleting 4 years earlier than a standard calculation would suggest.

Factors That Drain Savings Faster Than Expected

Several real-world pressures accelerate depletion in ways that standard assumptions miss.

Healthcare costs. The 2025 Fidelity Retiree Health Care Cost Estimate puts the average healthcare spending for a 65-year-old at $172,500 over a full retirement, not counting long-term care. The Medicare Part B premium rose 9.7% in 2026 to $202.90 per month, outpacing the Social Security COLA. Healthcare inflation is projected at 5.8% annually. Build this into your calculator inputs.

Longevity. According to TIAA Institute research, most Americans underestimate how long they will live. Only 32% of adults correctly answered a question about the life expectancy of a 65-year-old. Those who underestimate their lifespan save less and plan shorter timelines. The population over 85 is projected to double within 20 years. Plan for a longer life, not a shorter one.

Sequence of returns risk. Retiring into a down market, then withdrawing at a fixed rate, damages a portfolio permanently. You sell shares at low prices during the decline, leaving fewer shares to recover when markets rebound. A $1 million portfolio that drops 30% in year one of retirement loses far more in real impact than the same loss in year 20, because you are withdrawing from a smaller base for all the years that follow.

Early retirement. Retiring at 55 versus 65 adds 10 years of withdrawal and 10 fewer years of compounding. It also affects Social Security timing, often forcing a lower benefit if you claim early to bridge the income gap.

Inflation on fixed withdrawals. At 3% annual inflation, $5,000 per month today costs the equivalent of $9,030 per month in 20 years. A plan that looks comfortable at retirement age may look strained by age 82. Nearly half of retirees report that retirement expenses ran higher than expected, per Schroders' 2026 U.S. Retirement Survey.

How to Make Your Savings Last Longer

If your calculator shows a gap, these strategies make a measurable difference.

Delay Social Security. Delaying Social Security past your full retirement age increases your monthly benefit by 8% per year up to age 70. Claiming at 70 versus 62 can nearly double your monthly benefit. That higher guaranteed income reduces how much your portfolio must cover each month, which extends its life significantly.

Reduce your withdrawal rate in down years. Flexible withdrawal strategies, where you pull slightly less from your portfolio in years when markets fall, meaningfully extend how long savings last. Morningstar's research shows flexible strategies support starting rates up to 5.7%, versus 3.9% for fixed strategies.

Keep some equity exposure. Many retirees shift too heavily into bonds and cash, then watch inflation erode their purchasing power. Morningstar's research found the highest safe withdrawal rates occur at 30% to 50% equity allocations. A fully conservative portfolio often underperforms inflation over 25 years.

Control healthcare costs proactively. Choose Medicare Advantage or Medigap coverage carefully. A Medigap policy converts unpredictable out-of-pocket costs into a fixed premium, making budgeting more reliable. Consider a Health Savings Account (HSA) during your working years: contributions are tax-deductible, growth is tax-free, and qualified medical withdrawals are tax-free.

Consider part-time income in early retirement. Working part-time for even two to three years in early retirement, earning $20,000 to $30,000 per year, reduces the drain on your portfolio during the critical early years when sequence-of-returns risk is highest.

Downsize housing. A paid-off home reduces fixed monthly costs. If you own a home, downsizing at retirement frees equity, reduces maintenance costs, and lowers property taxes. For many retirees, this single move adds years to how long their savings last.

Frequently Asked Questions

How long should my retirement savings last?

Most financial planners target 25 to 30 years of coverage. A 65-year-old man can expect to live to around 83, while a woman of the same age can expect to reach 85 or older. Planning for 30 years, or to age 95, gives you a strong buffer against outliving your savings.

What is a safe withdrawal rate in 2026?

Morningstar's 2026 State of Retirement Income report recommends a 3.9% starting withdrawal rate for a 30-year retirement with a 90% probability of success. This applies to portfolios with 30% to 50% in equities. More flexible spending strategies can support rates up to 5.7%.

What inputs does a retirement savings calculator need?

Most calculators need your current savings balance, monthly spending in retirement, other income sources such as Social Security or a pension, expected rate of return on your investments, and an inflation rate assumption. Some also ask for your current age and target retirement age.

How does inflation affect how long retirement savings last?

Inflation erodes purchasing power every year. At 3% annual inflation, $5,000 per month in today's dollars costs nearly $9,000 per month in 20 years. A calculator that ignores inflation will overestimate how long your savings last.

What happens if my retirement savings run out?

You would rely entirely on Social Security, which paid an average of $1,877 per month in late 2024. For most people, that does not cover full living expenses. Running out of savings forces lifestyle cuts, reliance on family, or a return to work. The goal of planning is to prevent this outcome.

Does Social Security income affect my retirement savings duration?

Yes, significantly. Social Security reduces the amount you need to withdraw from your portfolio each month. A household receiving $3,000 per month from Social Security needs far less from savings than one receiving nothing. Always include Social Security estimates in your calculator inputs.

Can I withdraw more than 4% per year in retirement?

You can, but it increases the risk of running out of money. Morningstar's research supports up to 5.7% for retirees who adopt flexible spending strategies that adjust withdrawals when markets decline. Fixed-rate withdrawals above 4% raise depletion risk significantly over 30 years.

Conclusion

A how long will my retirement savings last calculator gives you the one number that matters most: how many years your money will cover you. Run the calculation with accurate inputs, test multiple scenarios, and treat the result as a planning tool, not a final verdict.

If your results show a gap, start with Social Security timing. Delaying from 62 to 70 is the single most powerful lever most retirees have. Then look at spending, investment allocation, and whether part-time income in early retirement changes the picture.

Run your numbers today. A free calculator from Fidelity, NerdWallet, SmartAsset, or Bankrate will take you five minutes and give you a clearer view of your retirement than years of guessing.

This article is for informational purposes only and does not constitute financial advice. Consult a qualified financial advisor for guidance specific to your situation.